How to Compare Lenders

THANK YOU for taking the time to educate yourself further on how to effectively compare lenders! That tells us you’re a conscientious consumer and just the kind of client we love to work with, so we’ll make this short and sweet:

The only way to effectively compare lenders, is to compare the interest rate being offered in conjunction with the sum of lender charges being quoted!!!

All of the other closing costs such as your escrow fee, title insurance, recording, transfer fees, ETC are going to be based on your local area’s prevailing market costs, and will be the same regardless of where you get your financing. For a detailed breakdown specific to your unique transaction, Click Here (custom rate quote link)

Here are a couple important things to bear in mind as you begin comparing lenders:

- Mortgage rates can and do change daily

- Interest rates typically are not locked in until you have chosen a property and a closing date

- Until your rate Is locked, some fees can vary based on market conditions

- Property type, debt to income ratio, credit scores, down payment, occupancy and several other factors will determine the final terms you will qualify for

Finally,

Your Mortgage is likely the biggest financial commitment you will make in your lifetime, so cheapest doesn’t always mean ‘BEST!’

But chances are, we’re going to beat most of the competition, provide you better education and make sure we have your transaction structured to best fit your unique needs!

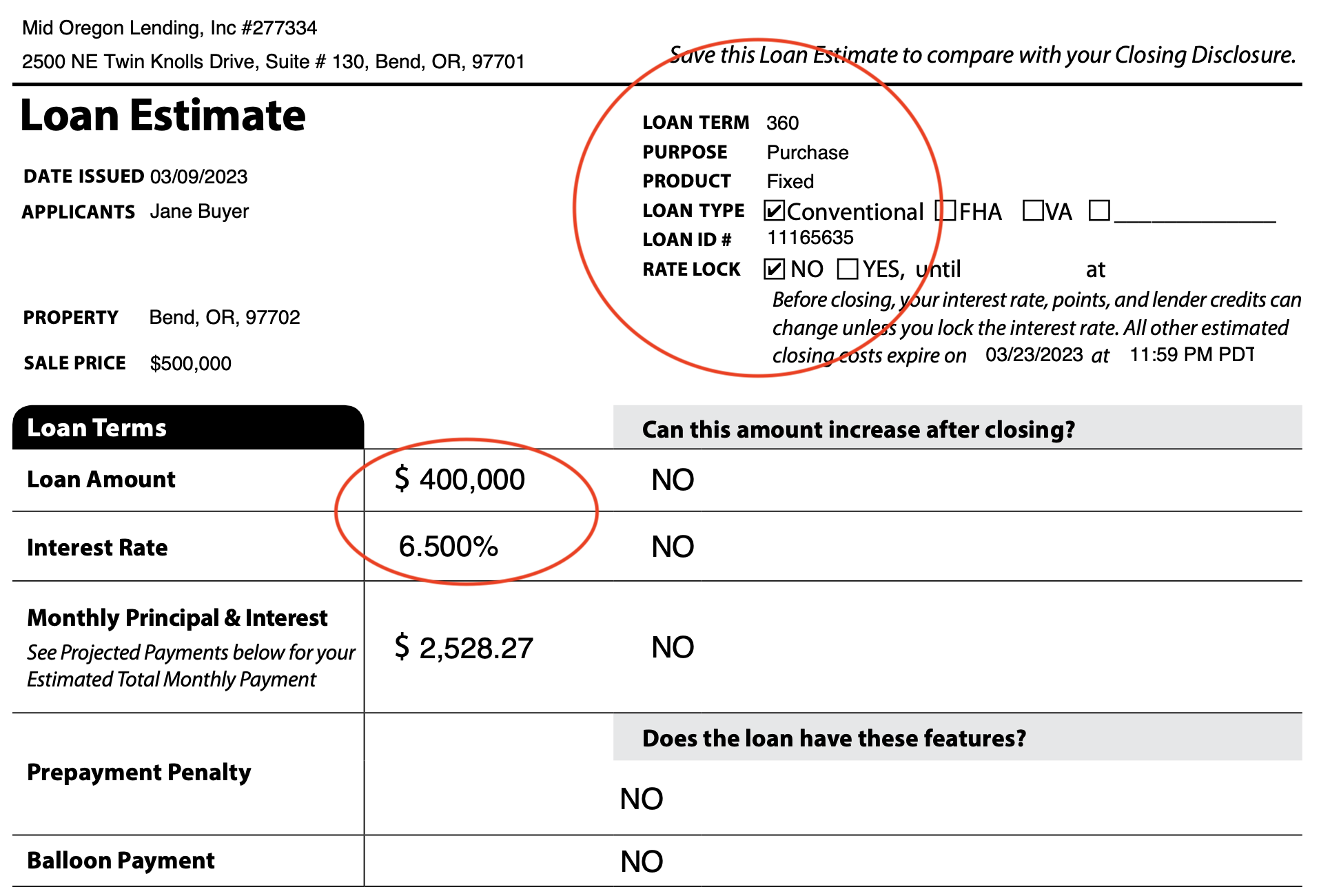

The industry standard document you should review is called a Loan Estimate (LE) and because interest rates can and do change daily, it’s important you compare LE’s prepared on the same day and at the same interest rate so you know you’re getting a fair comparison. Also make sure you’ve provided the same purchase price and loan amount with each lender and the same kind of loan. E.G. Conventional 30 year, VA, FHA, Etc.

On the top of the first page is a summary section that confirms the loan terms are the same and whether the rate is locked. Typically you will need to have a property identified and a close date determined before locking rates. Beneath the summary section you’ll see the loan amount and interest rate being quoted:

Further down the first page you’ll see the monthly taxes and insurance, the total payment, total closing costs, and final cash due at closing. Remember that until you have a property identifed, taxes and insurance will vary so don’t be fooled by artificially low quotes on this part of your total mortgage payment.

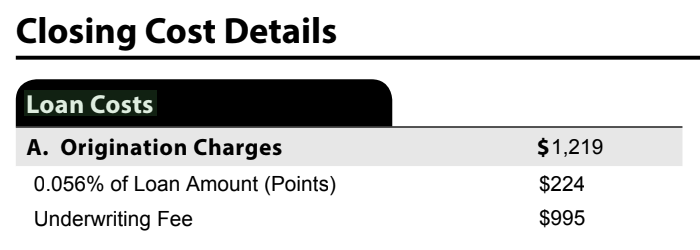

On page two in the upper left hand corner of the page is the “Meat and Potatoes” of this disclosure.

This is where you should be looking to accurately compare quotes!

The sum of the lender charges at the top of Section A in conjunction with the interest rate being quoted on page 1 is the most important comparison you should make.

In this example, there is a slight discount fee of $224 to get the 6.5% interest rate quoted and a typical underwriting fee. Some lenders may charge Origination fees, Processing fees, Admin Fees, application fees, Etc, but at the end of the day it’s the sum of those fees in lockstep with the rate being offered that should be your primary focus.

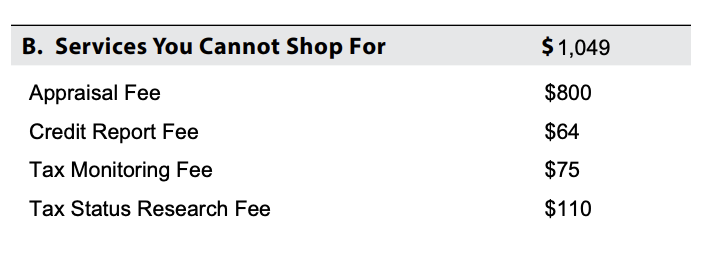

Section B lists the Third-Party Fees for services required to process and approve your loan, and the vendors that provide these services are typically chosen by the lender. You may see very slight differences from lender to lender but typically they will be fairly similar across the board:

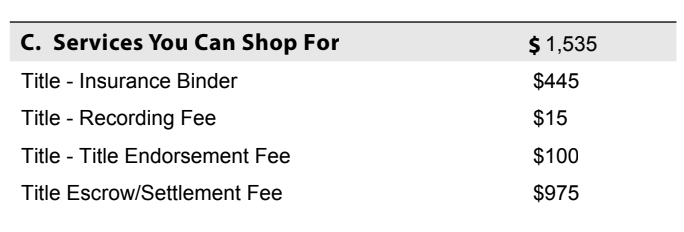

The next section in the LE itemizes your title and escrow fees. Again, don’t be fooled by fees quoted artificially low here just to make the cash to close figure look smaller. If you’ve chosen a property and provided the address to the lender, itemizing accurate fees here is as simple as us calling up the title and escrow provider on your transaction to confirm the charges:

Section D just beneath that sums up the total closing costs for your transaction. In effect, this is how much you are paying to get your loan.

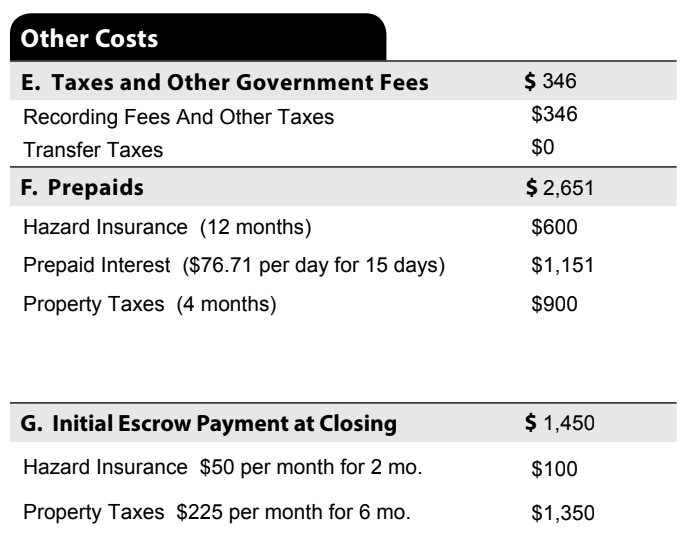

The top of the right hand column itemizes the other costs for Property taxes, Insurance, and Prepaid Interest and these costs will vary depending on what month and day you close your transaction. Sadly, many on-line or national lenders are not educated about properties in Oregon and may under-quote line items in this section to make their ‘bottom line’ look smaller.

IF you provide us with the property address, we can give you a very realistic expectation of what you should expect at closing in this section of the LE:

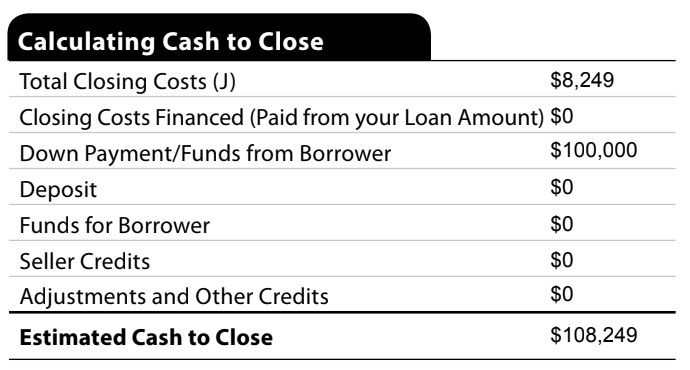

At the bottom of the right hand column you’ll see the total calculation of Cash needed at closing which includes your closing costs, pre-paid taxes and insurance, reserves deposited with the lender and your down payment.

The third page of the LE includes required disclosures about your transaction and other information and statistics about your loan, such as how much you’ll pay in interest and principal over the first five years of the loan and your Annual Percentage Rate, or APR.

The APR is a broad measure meant to indicate the ‘cost of credit’ over the term of your loan. Certain closing costs are added to the lifetime interest you would pay over 360 payments (assuming a 30 year loan) divided by the principal loan amount at closing.

Confusing? Just remember this: if there’s a large gap between the note rate being quoted on the first page and the APR on the third page, it’s an indication you may be paying too much for your loan!

If you’ve made it this far, CONGRATULATIONS on taking the bold first step in educating yourself on how to effectively compare Loan estimates. We’re grateful you’ve chosen to look into this in detail and look forward to earning your trust. Give us a call, drop us a line, or request a custom rate quote and we’ll look forward to hearing from you!